What are the Different Medicare Supplement Plans?

Medicare Supplement Insurance (also known as Medigap) can be a valuable piece of the Medicare puzzle. Medicare Supplement plans step in to help cover Medicare-approved expenses that Original Medicare (Part A and Part B) may leave you with.

Medicare Supplement Plans A – N offer different coverage based on your health care and financial needs. There are 10 standardized Medicare Supplement Insurance plans in 47 states. Wisconsin, Massachusetts and Minnesota have their own plans. So this means your Medicare Supplement coverage won’t differ state-to-state unless you live in one of the three just mentioned. This also means that your plan’s coverage won’t change based on the insurance provider you choose. Plus, you can apply for Medicare Supplement plans all year-round as long as you are eligible for Medicare. Just remember that your application may be subjected to underwriting if you apply outside of your initial enrollment period.

So, how can you decide which Medicare Supplement plan may be the right one for you? We’ll take a look at all of the Medicare Supplement plans to help you understand more about each option.

Medicare Supplement benefits plan overview

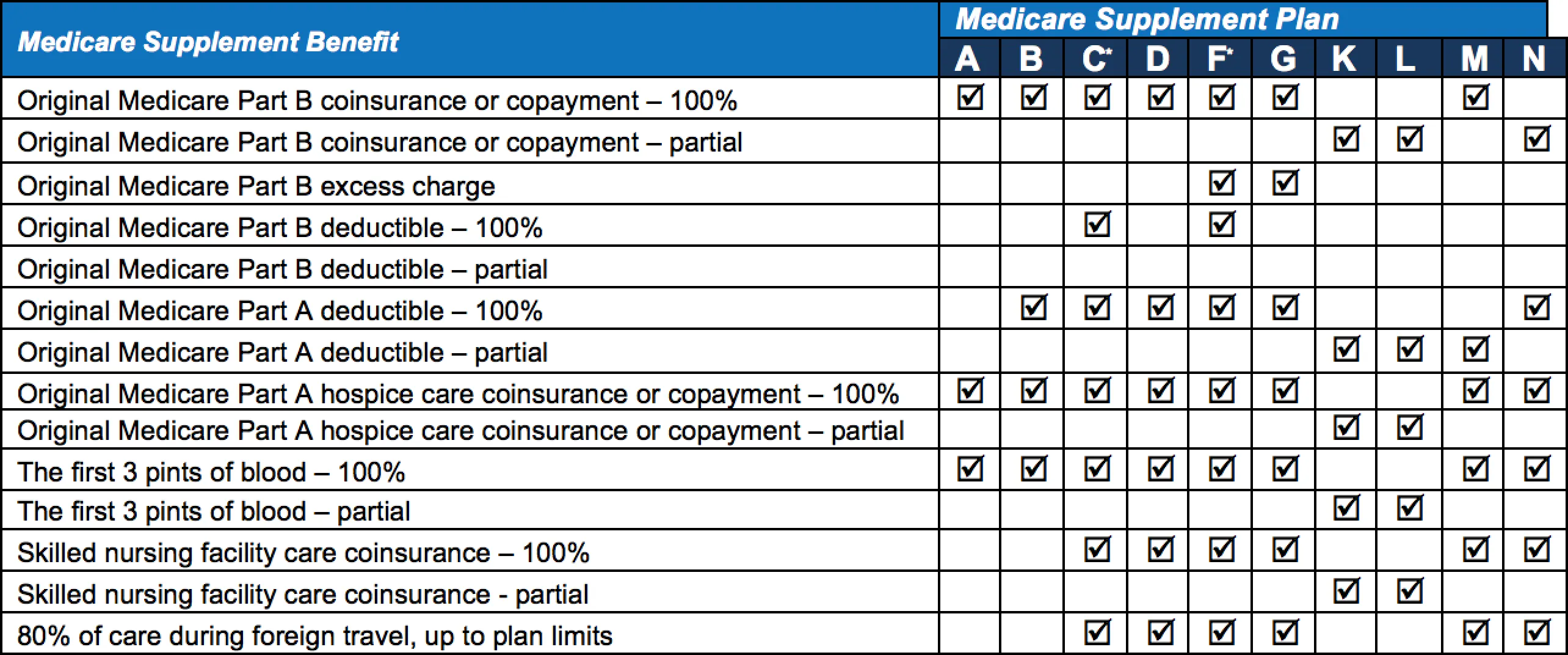

It’s hard to keep track of what each plan does and doesn’t cover. We’ll explain each plan in detail below, but here’s a chart to help you see what current plans are available, and what benefits they include.1

*Medicare Plans C and F are only available to those eligible for Medicare before Jan. 1 , 2020.

Medicare Supplement Plan A

Not to be confused with Original Medicare Part A, Medicare Supplement Plan A is the most basic Medicare Supplement plan. If Plan A covers it, then most of the others do, as well. Medicare Supplement Plan A (and every other Medigap plan) completely covers Medicare Part A coinsurance and hospital costs up to an additional 365 days after your Medicare Part A benefits reach their limit.

Medicare Supplement Plan A also covers:2

Original Medicare Part B coinsurance or copayment

The first 3 pints of blood

Original Medicare Part A hospice care coinsurance or copayment

Medigap’s Plan A and most of the other Supplement plans cover all of these expenses, but Medicare Supplement Plans K and L are a little different. We’ll discuss those in a bit.

Medicare Supplement Plan B

Medicare Supplement Plan B is very similar to Plan A. It offers one additional benefit – coverage for the Original Medicare Part A deductible.

Medicare Supplement Plan F

Medicare Supplement Plan F may seem like a strange place to move to next. Why not just keep working our way through the alphabet? The answer is that Plan F is the most comprehensive Medicare Supplement plan. But, while Plan F is very comprehensive, it’s slated to be phased out soon. People who become eligible for Medicare after January 1, 2020 won’t be able to select a Medicare plan that covers the Plan B deductible. That means that Plan F (as well as Plan C) will no longer be available to people who turn 65 on or after 1/1/2020. If you’re currently on one of these plans, your coverage won’t change. But newly-eligibles will need to find another option.

Plan F covers all of the benefits we’ve discussed already, but it also covers:3

Skilled nursing facility care coinsurance

Part A deductible

Part B deductible

Part B excess charge

80% of care during foreign travel, up to plan limits

There’s also a high-deductible version of Plan F. With this plan, you’ll pay all your Medicare-covered costs up to $2,870 before the plan pays for anything.

Medicare Supplement Plan C

Medicare Supplement Plan C is the other plan that will no longer be offered to those who become eligible for Medicare on or after 1/1/2020. It’s similar to Plan F. But Plan C doesn’t cover Plan B excess charges. What does that mean?

If you have Original Medicare, and a doctor or service provider is allowed to charge more than the Medicare-approved amount, that’s called the excess charge. Plan F protects against that, while Plan C doesn’t. Plan C does cover everything else a Medicare Supplement plan can, though. Bear in mind that it’s also going away for people who become eligible for Medicare after January 1, 2020.

Medicare Supplement Plan G

Medicare Supplement Plan G is perhaps the most similar plan to Plan F that will still be available once plan F is gone. It covers everything that Plan F does – except the Part B deductible. This plan even includes Part B excess charges. Once plan F is gone, Plan G will be the only plan that covers these charges. While it may not be as comprehensive as Plan F, Plan G is a very close second.

Medicare Supplement Plan D

Don’t confuse Medicare Supplement Plan D with Medicare Part D. Medicare Supplement Plan D is one of the more comprehensive options that will remain once Plan F and C are gone. If Plan G is similar to F, Plan D is similar to Plan C. This plan covers everything that Plan C does, except for that Part B deductible.

The only difference between Plan D and Plan G is that Part B excess charge coverage. So if you’re deciding between the two, your decision will likely depend on how important that excess charge coverage is to you.

Medicare Supplement Plans M and N

Medicare Supplement Plan M and Plan N are very similar to Plan D. In general, they cover the same charges. However, each plan comes with a limitation. Plan M only covers 50% of your Part A deductible. Meanwhile, to quote Medicare.gov, “Plan N pays 100% of the Part B coinsurance, except for a copayment of up to $20 for some office visits and up to a $50 copayment for emergency room visits that don’t result in inpatient admission.” All in all, these plans will cover the same types of expenses as Plan D. It’s just the amounts that differ.

Medicare Supplement Plans K and L

Medicare Supplement Plans K and L are a little different. As we mentioned earlier, they both cover a fraction of costs until you reach an out-of-pocket limit. For example, these plans only cover a small portion of the Part B coinsurance or copayment, the first 3 pints of blood, and Part A hospice care coinsurance or copayment. They also cover the same percentage of skilled nursing facility care coinsurance, and the Part A deductible. For Plan K, these expenses are covered at 50% until you reach the yearly out-of-pocket limit of $8,000. Plan L covers 75% of these expenses, until you reach an out-of-pocket yearly limit of $4,000. Once you hit that limit (and your yearly Part B deductible), the plan pays 100% of covered services for the rest of the calendar year.

Another limitation of these plans is that they do not cover any amount of medical expenses during foreign travel.

What’s the difference between Medicare parts and Medicare Supplement plans?

You may have noticed that some Medicare Supplement Insurance plans sound similar to the Medicare parts. For example, Medicare Supplement Plan A and Medicare Part A sound alike. But Medicare Parts vs. Medicare Supplement Plans are very different – from the benefits they offer to the ways they fit into your health care coverage puzzle. We break it down here.

Medicare parts vs. Medicare Supplement plans

Medicare Part A

Medicare Supplement Plan A

This is the first part of Original Medicare and is provided by the government. It covers emergency care you receive in the hospital, as well as inpatient nursing care and hospice care. Typically, you don’t pay a premium for this coverage.

Medicare Supplement Plan A covers Medicare Part A coinsurance and hospital costs up to an additional 365 days after your Medicare benefits are used. It also covers Part B coinsurance or copayment, the first 3 pints of blood, and Medicare Part A hospice care coinsurance or copayment.

Medicare Part B

Medicare Supplement Plan B

This is the second part of Original Medicare and is provided by the government. It covers doctor services, outpatient care and preventive services. There’s a monthly premium, which in 2026 is $202.90. However, this premium can vary based on your income.

Medicare Supplement Plan B has the same coverage as Medicare Supplement Plan A. However, this plan also includes Medicare Part A deductible coverage.

Medicare Part C

Medicare Supplement Plan C

This is also called Medicare Advantage. This plan is offered by private insurance companies, so there’s usually a separate premium you have to pay in addition to your Part B costs. Medicare Advantage plans cover everything that Original Medicare (Part A and B) covers, but with extra benefits like dental, vision and hearing health care services. Medicare Advantage typically includes Medicare Part D as well.

Medicare Supplement Plan C covers the same health care and services as Medicare Supplement Plan B. It also covers:

Medicare Part B deductible

Medicare Part A hospice care coinsurance or copayments

Medicare Part B copayments and coinsurance

Skilled nursing facility care coinsurance

Foreign travel emergency coverage (80% of approved costs)

Note: This plan will no longer be offered to people who were eligible for Medicare after January 1, 2020.

Medicare Part D

Medicare Supplement Plan D

This is also referred to as a Prescription Drug Plan (PDP). This plan is offered by private insurance companies, so there’s a separate premium you have to pay in addition to your Part B costs. Medicare Part D is prescription drugs coverage, but the drugs covered depend on your insurance provider.

Medicare Supplement Plan D covers everything that Plan C covers, minus the Medicare Part B deductible. If you’re eligible for Medicare after the January 1, 2020 cutoff date for Medicare Supplement Plan C, Medicare Supplement Plan D may be the next best option for you.

Which Medicare Supplement plan is right for you?

Medicare Supplement plans are available so that you can boost your Original Medicare health care coverage. All in all, these Medicare Supplement plans fall into a few broad categories. Medicare Supplement Plans A and B are cost-conscious but provide minimal coverage. Plans K and L are cost-conscious, but come with an out-of-pocket max that must be met. Plans F and C are comprehensive, with only one major difference between them. Plans G and D nearly mirror F and C, but don’t cover the Part B deductible. Plans M and N offer similar coverage to D, but offer less coverage for specific expenses.

Your Medicare Supplement Insurance plan coverage won’t vary based on the insurance provider you choose. However, only you can decide which of these plans best suits your needs. But with all of the different coverage available, the chances are good that you can find a plan that works for you.

Sources

1,2,3 Medicare.gov. Web page: How to compare Medigap policies. Accessed 12/03/2024 from www.medicare.gov/supplements-other-insurance/how-to-compare-medigap-policies

Item# 453029

Suggested content for you in Medicare

-

How to Choose the Right Medicare Supplement Insurance Plan

-

Hospital Indemnity Insurance 101: Coverage, Costs and Key Benefits

-

Are High Deductible Medicare Supplement Plans Right for You?

-

Medicare Supplement Plan G vs. Plan N: Which One’s Best for You?

-

Understanding Your Prescription Drug Plan Under Medicare Part D

-

What Is Medicare Supplement Plan F and Is It Still Available?

-

Medicare Supplement Plan C: Your Guide to Comprehensive Coverage

-

How Does Medicare Supplement Insurance Work with Original Medicare (Part A and B)?

-

Medicare Advantage vs. Medicare Supplement Insurance Plans — Which Is Right for You?

-

A detailed look at what’s covered under Medicare Part B

Explore other topics

Traveling in Retirement

Top 5 Cities for Seniors to RetireStaying Fit

5 Exercises for a Cardio Workout At HomeHealth & Aging

Fun Activities for Seniors to Stay Healthy